The main role of forensic accountants is to assist the courts, solicitors and clients understand...

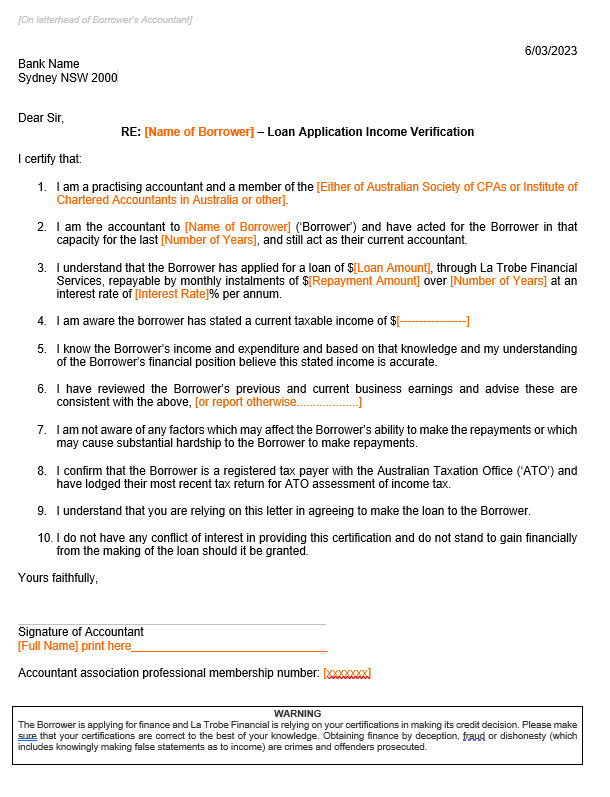

When clients apply for a loan or other financing, they may be required to provide an "accountant's letter" from a professional accountant as part of the application process. This letter verifies the accuracy of the client's financial statements and includes details about their financial status. While providing an accountant's letter can be a valuable service for clients, it can also present various legal risks for the accountant.

We'll discuss some of the significant legal risks that come with writing letters for financing applications.

1. Liability for false statements

Accountants, being professionals with expertise in financial matters, are often called upon to provide opinions and recommendations through letters, reports, and other forms of written communication. The accuracy and reliability of these statements are of the utmost importance, as they are used by various stakeholders, such as clients, banks, investors, and government authorities, to make important financial decisions.

If an accountant makes false or misleading statements in a letter, they may be held liable for the damages that result from these statements. This liability can take various forms, including monetary damages, reputational damage, and even legal action.

2. NegligenceIf the accountant fails to exercise due diligence in preparing the letter, meaning they do not take the necessary steps to ensure the accuracy and reliability of the information in the letter, they may be held liable for professional negligence.

3. Conflict of interest

It is important for accountants to recognise and manage conflicts of interest to maintain the integrity of the profession and protect the interests of their clients and other stakeholders. This can be done by disclosing any potential conflicts of interest to all parties involved, avoiding situations that could lead to conflicts of interest and ensuring that professional judgment is not influenced by outside factors.

4. Breach of confidentiality

As an accountant, one is entrusted with sensitive financial information and is expected to maintain the privacy of that information. A breach of this confidentiality, either through intentional or accidental means, can result in serious consequences for both the client and the accountant.

5. Violation of professional standards

Professional standards are violated if an accountant fails to adhere to these established guidelines in their work. This can include issues such as misstating financial information, failing to follow proper accounting procedures, or providing inadequate disclosure in financial reports.

While providing an accountant's letter can be a valuable service for clients, it is important for accountants to be aware of the legal risks associated with this task. Accountants should ensure that any letter they provide is accurate, complete, and in compliance with all relevant laws and regulations related to privacy and data protection. They should also be aware of their professional obligations and avoid giving opinions on creditworthiness. It is also important to consult with legal counsel to ensure compliance and minimise risks.

Looking for a trusted partner to help you navigate your Accountant's Letter? Contact us today to become a client and let us guide you to success.

This blog has been prepared for the purposes of general information and guidance only. It should not be used for specific advice or used for formulating decisions under any circumstances. If you would like specific advice about your own personal circumstances, please feel free to contact us on 02 9411 5422. We can help make sure the right method is used to give you the maximum possible tax deduction associated with any of these methods.